Jul 14, 2015

CPI Europe Column edited by Anna Tzanaki (Competition Policy International) & Juan Delgado (Global Economics Group) presents:

The Economics of the UPS/TNT Case Revisited: Implications for the Future by Enrique Andreu, Jorge Padilla & Nadine Watson (Compass Lexecon)

Intro by Anna Tzanaki (Competition Policy International)

With the Commission’s prohibition decision on the UPS/TNT merger recently published, a comment on the economic analysis of the case is quite timely. This is an important decision as it has been the first time that efficiencies were considered of the size and quality capable to outweigh any anticompetitive effects of the transaction, at least in some of the affected markets, and also to be passed-on to consumers. The authors closely examine the Commission’s analytical approach focusing on price concentration models and assessment of efficiencies. This analysis is important for another reason: the same framework may be used to assess the proposed FedEx/TNT merger, which is set to be decided next month. We hope you delve into the discussion and enjoy reading!

Two years ago, the European Commission blocked the UPS/TNT merger2. The public version of the European Commission decision was published only recently, on 12 May 2015. This note summarises and assesses the main analyses done in that case, and then considers the likely implications of the application of that analytic framework for the proposed FedEx/TNT transaction and any other transaction in the same relevant markets.

The Commission’s overall analysis

The Commission reviewed the UPS/TNT transaction focusing on the market for international express deliveries of small packages in the EEA. The Commission distinguished two types of players in the market: integrators and non-integrators.

Integrators were defined as operators with an international integrated air and ground small package delivery network. This implies having control of (i) extensive aircraft fleets which allows moving small packages quickly over long distances; and (ii) ground networks made up of road vehicles and sorting centres. According to the UPS/TNT decision, there are only four operators in Europe that meet this description: DHL, UPS, FedEx and TNT Express.

The Commission found that the UPS/TNT transaction would significantly reduce competition as the number of integrators would have been reduced from four to three, and that the new entity would not be significantly constrained by non-integrators, new entry or customer bargaining power. As a result, the Commission concluded that the merger would likely result in price increases in 25 EEA countries for intra-EEA express services3.

The Commission accepted that certain efficiencies would arise. In 10 of the 29 EEA countries the Commission concluded that UPS’ verified efficiencies would outweigh the predicted gross price increases and these intra-EEA express markets (representing mostly the major markets) were therefore found to be unproblematic as were another four countries4. However, the Commission Considered the efficiencies were insufficient to outweigh the predicted price increases in the other 15 EEA countries.

The Commission considered new market entry unlikely. According to the Commission’s decision, the providers of deferred services are unlikely to be able to quickly launch express services, even if they had incentives to do so. Customer buying power was also unlikely to be an effective constraint on pricing as, according to the Commission, integrators are able to identify customers that are unlikely to consider deferred services as a suitable alternative and would therefore more easily accept a price rise for express services. The existence of customers that would be willing to substitute express and deferred services would not offer any protection to those that are unable or unwilling to switch.

The approach used to assess the net price effect of the transaction

We turn now to examine more closely the Commission’s analysis. In its analysis of the effects of the UPS/TNT transaction, the Commission conducted an analysis that allowed balancing the pro-competitive and anti-competitive effects of the transaction.

The analysis consisted of three parts:

(i) an estimation of the likely impact of the merger on prices;

(ii) an estimation of the likely efficiencies and an assessment of whether these efficiencies outweighed the likely price effects; and

(iii) an overall assessment of the change in market conditions in countries where the efficiencies did not clearly outweigh the estimated price increases.

The Commission’s price-concentration approach in UPS/TNT should be the basis for the analysis of the likely price effects of other proposed transactions in the market for international express deliveries of small packages in the EEA, and more generally, to assess the effects of transactions in other concentrated markets.

First, in order to estimate the likely price impact from the merger, the Commission conducted a price-concentration analysis. This type of analysis allows testing the conclusions of static economic models of oligopolistic competition, which predict that mergers between companies producing imperfect substitutes are likely to lead to price increases. This is because, following a price increase, the new entity will be able to recapture, through the sales of the merging partner’s products, part of the sales that would have been otherwise lost to a competitor as a result of such price increase. This effect is stronger if the merger brings together close competitors and/or if the concentration on the market is already high pre-merger5.

| The Commission’s price-concentration approach in UPS/TNT should be the basis for the analysis of the likely price effects of other proposed transactions in the market for international express deliveries of small packages in the EEA, and more generally, to assess the effects of transactions in other concentrated markets. |

In the UPS/TNT transaction, the Commission quantified the extent to which prices of intra-EEA express services varied depending on the number of competitors across lanes. When analysing the likely impact of the merger on the prices of the merging parties, the Commission took into account that the price per kg (of End-Of-Day (“EOD”) products) depends on cost, distance, market size, customer size as well as on the presence of competitors. This analysis was conducted using actual data from the merging parties on their historical prices for all intra-EEA origin-destination lanes. The Commission used more than a million pricing points for its analysis. The Commission quantified the predicted price effects for 25 EEA countries6.

The results of the Commission showed that prices were higher on lanes where fewer competitors operated, even where DHL had strong presence7. In particular, the Commission’s price-concentration results showed that a four to three merger in the intra-EEA express delivery market was likely to lead to significant price increases (i.e., between 5% and 20%) in 12 countries, including Greece, Malta, the Baltic States (Estonia, Latvia, and Lithuania), Slovenia, Bulgaria, Romania, Poland, Slovakia and Scandinavia (Finland and Sweden). In the remaining 13 countries the predicted price increases were below 5%. UPS has appealed the Commission’s decision, arguing inter alia that the Commission used incorrect inputs and made procedural errors. But to the best of our understanding, UPS has not challenged the use of a price-concentration model per se.

Second, the Commission analysed the efficiencies likely to be generated by the transaction following recital 29 of the Merger Regulation:8

“In order to determine the impact of a concentration on competition in the common market, it is appropriate to take account of any substantiated and likely efficiencies put forward by the undertaking concerned. It is possible that the efficiencies brought about by the concentration counteract the effects on competition, and in particular the potential harm to consumers, that it might otherwise have and that, as a consequence, the concentration would not significantly impede effective competition […].”

For the first time efficiencies were a decisive factor in eliminating competition concerns in markets which actually accounted for the vast majority of the business by value. The Commission analysed the parties’ calculations of the expected efficiencies derived from the transaction and considered that the only efficiencies sufficiently substantiated and reliable were those concerning the estimated cost savings in European air network and ground handling costs. The Commission only considered efficiencies arising within three years after the merger as capable of offsetting likely price increases.

| For the first time efficiencies were a decisive factor in eliminating competition concerns in markets which actually accounted for the vast majority of the business by value. |

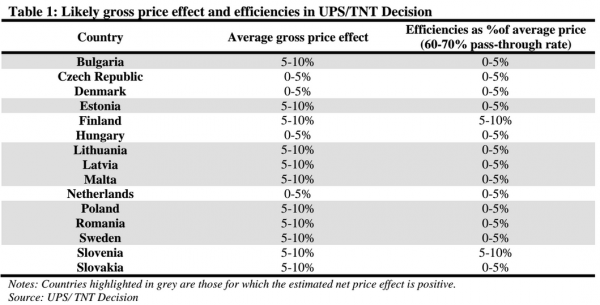

The Commission allocated the overall cost savings to individual lanes with origin and destination within the EEA, proportional to each lane’s share of UPS’ total European air transport costs and applied a pass-through rate of 60-70%. The pass-through rate was obtained from the price-concentration models estimated by the Commission and captures the proportion of cost changes that are passed-on to prices charged to customers. The estimated cost savings ranged between 5% and 10% of the price in 5 countries and between 0% and 5% of the price in the remaining countries.

According to the Commission’s results, efficiencies outweighed the likely price increases in 10 EEA countries. In these countries with likely net price reductions, the Commission also found that FedEx was a significant player. These intra-EEA express markets were therefore found not to be problematic as were a further four.

In the third step of the analysis, the Commission identified the remaining 15 countries where accepted efficiencies did not offset the likely price increases and for each of these it conducted an overall assessment. For 8 out of the remaining 15 countries, the Commission found a clear positive net price effect (see Table below). The Commission considered these markets problematic without need for further analysis.

While in the other 7 countries (i.e., Czech Republic, Denmark, Finland, Hungary, Netherlands, Slovenia, and Slovakia), the net positive effect was negligible, neutral or even negative, the Commission still included them in the list of countries where the merger was likely to have adverse economic effects. For these seven countries the Commission performed an overall assessment of market conditions and found that notwithstanding the fact that predicted net price effects were negligible, other market factors pointed towards a likely significant impediment to effective competition. The key market factor was the role played by FedEx; the Commission considered that in these markets FedEx would not exert a significant market pressure to counteract the price increases, even in countries where it planned to expand (Denmark, Finland and Hungary) or already had high coverage (Netherlands).

Assessing the Commission’s analytical approach in UPS/TNT

A price-concentration analysis provides a well-grounded, clear and systematic approach to estimating likely price effects in the small package international express delivery market and balancing the likely estimated price increases against the expected efficiency gains. We regard the approach followed by the Commission in the UPS/TNT decision as a clear step forward in the analysis of potential anti-competitive effects in mergers occurring in concentrated industries. It offers an objective framework, based on sophisticated economic analysis, to balancing anti-competitive effects arising from the increase in concentration and pro-competitive effects resulting from merger-specific cost savings likely to be passed on to consumers.

The (limited) recognition of efficiencies, sufficient to clear 10 major markets, represents a significant breakthrough in the Commission’s approach to efficiencies, as for the first time efficiencies were a decisive factor in eliminating competition concerns in markets which actually accounted for the vast majority of the business by value. In our view, the Commission’s price-concentration approach should be the basis for the analysis of the likely price effects of other proposed transactions in this market, and more generally, to assess the effects of transactions in other markets likely to lead to significant cost savings and for which balancing likely anti-competitive effects and efficiencies is critical.

Implications for the proposed FedEx/TNT transaction

In our opinion the Commission’s assessment of the notified FedEx/TNT transaction will have to consider the likely effects of the transaction on the small package international intra-EEA express delivery market in the EEA, where the transaction will again reduce the number of integrators from four to three.

It is worth noting that in the UPS/TNT decision, the Commission considered 12 out of the 27 Member States non-problematic, in other words 75% of the EU business which would need to be considered in light of the new transaction, bearing in mind that FedEx was already a significant participant in those markets at the time, and has grown over the last three years. Other markets such as extra-EEA express delivery were also four to three markets but not covered closely in the decision of the UPS-TNT merger; these would have to be re-assessed for other combinations. Domestic express delivery markets may also need further assessment.

In the FedEx/TNT transaction, as in the UPS/TNT investigation or any other merger review in a highly concentrated market, the Commission will investigate the likely net price effect resulting from the transaction. Leaving aside any efficiency gains, judging from the conclusions of the Commission’s analysis of the market in the UPS/TNT transaction, the elimination of competition between TNT and FedEx is likely to result in higher prices even in the presence of DHL, UPS and other fringe competitors9. The consideration that one player may be somewhat smaller in particular Member States does not prevent the combination being problematic (and in any event, FedEx is not smaller than the other integrators in at least 9 of the major markets examined in UPS/TNT). The Commission will thus need to analyse whether claimed efficiencies are sufficiently verifiable and large to overcome the likely gross price increases caused by the removal of a close competitor, even if not the largest and most dynamic one10.

Click here for a PDF version of the article

1 The authors are economists at Compass Lexecon and advise UPS on competition economics matters. The opinions in this paper are, however, the authors’ sole responsibility and do not necessarily represent the views of UPS or other Compass Lexecon experts.

2 Case No COMP/M.6570 – UPS/ TNT EXPRESS.

3 The Commission did not quantify the predicted price effect for Ireland and Cyprus (due to lack of data) and for Norway and Iceland.

4 These are Cyprus, Ireland, Norway and Iceland.

5 Case No COMP/M.6570 – UPS/ TNT EXPRESS, para. 722.

6 The Commission did not use the price-concentration model to quantify the price effects in four countries: Cyprus and Ireland (due to lack of data) and Norway and Iceland. See para. 739 of the Decision.

7 See para. 725 of the Decision.

8 Council Regulation (EC) No 139/2004 of 20 January 2004 on the control of concentrations between undertakings (the EC Merger Regulation), para.29.

9 See para. 726 of the Decision.

10 See para. 720 of the Decision.

Featured News

DOJ and FTC Introduce Website for Reporting Anti-Competitive Healthcare Practices

Apr 18, 2024 by

CPI

US Congress Advances Legislation to Compel TikTok Sale

Apr 18, 2024 by

CPI

UK Financial Sector Advocates Enhanced Regulatory Accountability

Apr 18, 2024 by

CPI

Google and All 50 States Defend $700 Million Consumer Settlement

Apr 18, 2024 by

CPI

Colorado Enacts First Law to Protect Consumer Brainwave Data

Apr 18, 2024 by

CPI

Antitrust Mix by CPI

Antitrust Chronicle® – China Edition – Year of the Dragon

Apr 16, 2024 by

CPI

Review Logic and Rules for Concentrations of Undertakings that Do Not Meet the Standard of Notification

Apr 16, 2024 by

CPI

China’s Review of Semiconductor Transactions

Apr 16, 2024 by

CPI

Key Challenges and Tips for Merger Control Filing in China for Listed Companies

Apr 16, 2024 by

CPI

Key Point Review: China SPC Antitrust Judgments in 2023

Apr 16, 2024 by

CPI