The UK Energy Market Investigation: A Desperate Search for Evidence of a Lack of Competition?

Apr 15, 2014

CPI Europe Column edited by Anna Tzanaki (Competition Policy International) presents:

The UK Energy Market Investigation: A Desperate Search for Evidence of a Lack of Competition? by Frank Maier-Rigaud, Sean Gammons and George Anstey (NERA Economic Consulting)*

Intro by Anna Tzanaki (Competition Policy International)

Our April edition of the Europe Column is dedicated to the recent and hotly debated issue of the UK energy market investigation. With Ofgem, the sector regulator, proposing a reference to the CMA for an in-depth investigation of the market that could take up to a couple of years, stakes are high. This is not the first time that there is an inquiry into the energy sector. Political and consumer protection concerns have often challenged the industry setting. The authors explore these issues and also assess the authorities’ argumentation justifying the proposed market investigation from a competition perspective. The authors argue that the claimed lack of competition is not supported by compelling empirical evidence. Bearing in mind that regulatory intervention had also played a role in distorting competition, they stress the need for consistent and clear theories of harm put forward by the regulators. Therefore, they advocate caution when it comes to UK market investigations which may entail remedies and create uncertainty for the business community.

Introduction

The UK government progressively privatized the British gas and electricity industry between 1986 and 1996.1 By 2002 the British energy regulator Ofgem, had first made all customers eligible to choose their supplier and finally lifted price controls for all customer types, driven by the belief that competition would reduce prices.2 As Ofgem explained at the time:

“competition is now well established, effectively protecting customers’ interests, and continuing to develop well.”3

In the last six years, however, Ofgem has started to doubt its own prior assertions and has launched a number of detailed investigations into the sector. These comprise the 2008 Energy Supply Probe, the 2010 Retail Market Review but also the recent joint efforts together with the Office of Fair Trading (OFT) and the Competition and Markets Authority (CMA) in preparing the ground for an energy market investigation.4 While UK market investigations have a reputation for being primarily motivated by political concerns and therefore often serve the role of a pressure valve, the current debate in the UK is exceptional for its lack of faith in the competitive process. Announcements of new energy tariff policies by the Prime Minister and promises by the leader of the opposition to introduce a two-year price freeze if he comes to power are only the tip of the iceberg. On 27 March 2014, Ofgem launched a consultation on referring the market to the CMA for an independent and full-scale market investigation, which would take at least 18 months and will not only bind resources at the CMA but also cost the energy sector millions of Euros.5

The evidence of competition problems in the sector is in stark contrast to these developments. This was not changed by Ofgem’s proposal for a full-scale investigation.6 Indeed, the concerns presented are at best a list of theoretical possibilities as the limited empirical evidence mentioned in support of Ofgem’s concerns is consistent with both the presence of competition and its absence.

Evidence of a Lack of Competition: Market Outcomes

Much of the focus of the relevant Ofgem investigations has been on the structure of the industry and, in particular, the position of the “Big Six” and concerns over whether the incumbents were frustrating entry. The “Big Six”-epithet describes the vertically-integrated gas and electricity companies that emerged from the vertically-separated regional electricity supply boards and generation companies subsequent to privatization: British Gas (Centrica), EdF Energy, npower, E.ON UK, Scottish Power and SSE. These companies hold around 95 per cent of the customers in the domestic supply market, with lower shares in the non-domestic market especially for gas, and around 74 per cent of electricity generation.7

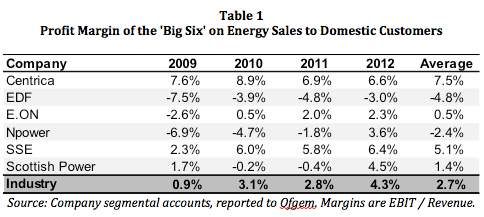

Indicative of the low quality of the debate, the largest public controversy has been over industry profits. Profits in the supply segment have been rising over the last few years, albeit from unexceptional levels; margins in energy supply in 2009 were around 0.9% on sales and rose to 4.3% in 2012, averaging 2.7% over the period (see Table 1, below). Profits have been even lower over the longer term. Data before 2006 is not publicly available, but Ofgem reported in 2011 that profits were 1.6% between 2005 and 2010.8 These profit levels are below Ofgem’s benchmarks for the sector: Ofgem has previously estimated a 3 per cent profit margin would be necessary for a “fully internally hedged [vertically integrated] utility” and up to 9 per cent for suppliers without any generation portfolio. Despite accusations that companies are squirrelling away profits in their generation segments, the most recent analysis of Ofgem, the OFT and the CMA suggests that “the generation sector is covering its cost of capital but no more.”9

Irrespective of the fact that the empirics are not matching the rhetoric, there exists no theory of harm anchored to a finding of high profitability under competition law. While the charging of excessive prices10 by a dominant firm is a possible, albeit controversial, theory of harm, such excessive prices are only indirectly related to high profits. In any case, even if the focus on profits is generously viewed as shorthand for excessive prices, such an abuse requires first and foremost dominance. While the UK energy sector with its six firms would probably not even pass as tight oligopoly, it is clear that single firm dominance can be excluded.

Evidence of a Lack of Competition: Market Features

If the evidence for a lack of competition in the sector is unclear, similar doubts pervade the authorities’ claims about the features of the market that lead to allegedly anticompetitive outcomes. The State of the Market Assessment (SMA) sets out five market features that it describes as providing evidence of a lack of competition in the sector.

First, the SMA conducts a lengthy examination of market segmentation and the separation of the customer base into different customer types. Customers who remain with their incumbent supplier (and may have never switched) are less likely to switch than customers who are with an entrant supplier in their area. Unsurprisingly, the least active participants in the market (so-called “sticky customers”) tend to pay higher prices as a result of not seeking out the best deals. Of course, switching in itself is irrelevant for assessing competition in a market and high and low switching rates are equally compatible with competition.11 In markets with high switching costs, entrants have to offer lower prices than incumbents in order to obtain market share and price differentials can indicate the presence rather than the absence of competitive pressure.

Second, the SMA contains a review of possible tacit coordination, an innovative theory of harm that has been considered in the past already in the aggregates market investigation but has also recently been invoked by the European Commission.12 The evidence shows that the companies raised prices at similar times (so-called “parallel pricing”). In the energy industry, where companies face common wholesale market and network costs, parallel pricing is equally plausible as an outcome of competitive behavior, where competing firms simultaneously raise prices in response to cost shocks.

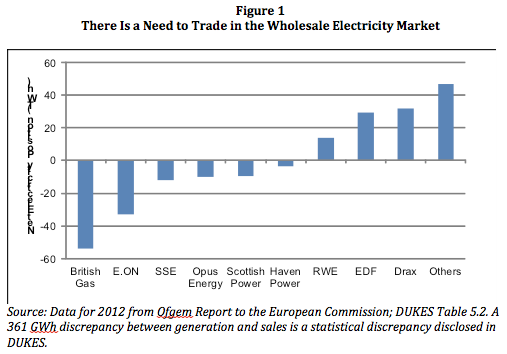

The third and fourth market features investigated in the SMA are barriers to entry and expansion and vertical integration. In principle, vertical integration between electricity generation and supply may constitute a barrier to entry by reducing liquidity on the wholesale market and the availability of electricity to entrant suppliers. Vertical integration was indeed also a major concern in the context of the EU Energy Sector Inquiry.13 In practice, however, the “Big Six” have large imbalances between the volumes they buy and sell (see Table 1), so that liquidity is hardly an issue. Moreover, as the authorities themselves recognize, vertical integration can bring real cost-reducing benefits in increasing the credit-worthiness and reducing the collateral requirements of supply businesses. Indeed Ofgem itself has previously argued that vertically integrated companies may be able to earn profit margins around one-third of those of independent companies.14

The fifth market feature investigated in the CMA is weak customer pressure. According to surveys commissioned by Ofgem, one in ten customers were not aware they could switch. Nonetheless, the evidence from consumer surveys seems largely inconclusive. Over half the customers who had never switched said it was because they were happy with their existing supplier.15

Conclusion

Ever since market investigations and sector inquiries have become part of the standard repertoires of the European Commission and the major national competition authorities in Europe, UK market investigations have drawn attention. The sector inquiry tool of the European Commission, for instance, has as its sole purpose the collection of information in order to give effect to the relevant competition articles of the Treaty. The inquiry itself is not a substitute for bringing a competition case against companies if indeed competition problems are identified. By contrast, market investigations in the UK not only gather information but conclude with more or less extensive structural and behavioral remedies. At least in the past these remedies were not always based on explicitly articulated objections based on a clear theory of harm. As a result, quite a few of the remedies imposed would typically not have survived the legal and procedural scrutiny otherwise standard in individual competition cases. Part of the reason for this may be the amalgamation of consumer protection and competition concerns. It may, however, also be partly due to the broad powers of the market investigation instrument. Recent efforts to impose some discipline, including forcing the authority to lay out a clear theory of harm, bring the instrument closer in line with the procedural safeguards and rights of defense also observed in individual competition cases. But the upcoming energy market investigation may put even these limited restraints to the test. It remains to be seen whether the CMA will be willing to go out on a limb based on the often unfounded and confused statements about what is wrong in the British energy market, or whether it will restrict its assessment to sound economic analysis.

In addition to the competition concerns presented in the document, Ofgem, the OFT and the CMA seem to have understood that the burden of regulation has added to barriers to entry in the market in recent years. The high costs of compliance keep small suppliers out and exemptions from regulations for small suppliers discourage entrants from growing. Moreover, as the three regulators stated in the SMA:

“In addition to the regulatory barriers to entry, the industry is affected by a high degree of policy change, political and media scrutiny, and negative publicity. As part of our assessment, we spoke to a number of firms that had previously considered entering the retail energy market. A consistent reason for not entering was the political environment surrounding the energy market and uncertainties surrounding the future course of policy.”16

The market investigation tool gives the CMA great power in the context of the British market. The energy market investigation is an opportunity for the newly instituted CMA to demonstrate that it will make judicious use of those powers. The CMA must demonstrate that it will only impose proportional remedies and that the necessity of the remedies is based on a comprehensive and thorough scrutiny of the relevant markets and a clear and straightforward theory of harm.

(Click here for a PDF version of the article.)

* Frank Maier-Rigaud is head of Competition Economics Europe at NERA Economic Consulting, Brussels, Berlin and full professor of Economics at IESEG (LEM-CNRS), Paris. Disclaimer: Frank Maier-Rigaud was responsible for the sector inquiry tool of the European Commission for many years and in that function was also involved in the EU energy sector inquiry. Any views presented are entirely his own.

Sean Gammons is head of Energy Team in London at NERA Economic Consulting, London.

George Anstey is Senior Consultant at NERA Economic Consulting, London.

1 For a history of privatisation in the British energy industry, see Simmonds, G. (2002), Regulation of the UK Electricity Industry, 2002 edition, Centre for the Study of Regulated Industries.

2 See descriptions in Ofgem (2004), Domestic Competitive Market Review 2004, A review document, April 2004, para 1.17, available at: https://www.ofgem.gov.uk/ofgem-publications/38538/6757-dcmr-publication-ch-1-3.pdf; Ofgem (2002), Future regulation of domestic gas and electricity supply markets – final proposals, February 2002, available at: https://www.ofgem.gov.uk/ofgem-publications/76206/1096-factsheet030215feb.pdf.

3 Ofgem (2001), Review of domestic gas and electricity competition and supply price regulation: Evidence and initial proposals, November 2001, Executive summary.

4 See Ofgem, OFT, CMA (2014), State of the Market Assessment, 27 March 2014, available at: https://www.ofgem.gov.uk/ofgem-publications/86804/assessmentdocumentpublished.pdf.

5 Ofgem (2014), Consultation on a proposal to make a market investigation reference in respect of the supply and acquisition of energy in Great Britain, 27 March 2014, available at: https://www.ofgem.gov.uk/ofgem-publications/86807/consultationpublish.pdf.

6 See for instance, NERA (2014), Energy Market Insights: Tantalus and Other Myths of the British Energy Market, March 2014, page 3, available at: http://www.nera.com/nera-files/NL_EMI_0314_Issue10.pdf.

7 Ofgem (2013), National Report to the European Commission, pages 50-60, available at: https://www.ofgem.gov.uk/ofgem-publications/82755/2013greatbritainandnorthernirelandnationalreportstotheeuropeancommission.pdf.

8 Ofgem (2011), The Retail Market Review – Findings and initial proposals, Supplementary appendices, ref: 34/11, 21 March 2011, page 40, available at: https://www.ofgem.gov.uk/ofgem-publications/39709/rmrappendices.pdf.

9 Ofgem, OFT, CMA (2014), State of the Market Assessment, 27 March 2014, page 120, para 6.79.

10 See OECD (2012) Excessive Prices, OECD Best Practice Roundtables in Competition Policy, October 2011, Background note prepared by Frank Maier-Rigaud for the OECD secretariat, available at: http://ssrn.com/abstract=1946779.

11 See OFT (2003) Switching Costs, Report prepared by NERA, available at: http://www.oft.gov.uk/shared_oft/reports/comp_policy/oft655.pdf.

12 See UK Competition Commission (2014) Aggregates, cement and ready-mix concrete market investigation, available at: http://www.competition-commission.org.uk/our-work/directory-of-all-inquiries/aggregates-cement-ready-mix-concrete and European Commission – IP/13/1144 22/11/2013, available at: http://europa.eu/rapid/press-release_IP-13-1144_en.htm.

13 See DG Competition report on energy sector inquiry SEC(2006)1724, 10 January 2007, available at: http://ec.europa.eu/competition/sectors/energy/inquiry/index.html.

14 See Ofgem, OFT, CMA (2014), State of the Market Assessment, 27 March 2014, page 14, para 1.38.

15 See Ofgem, OFT, CMA (2014), State of the Market Assessment, 27 March 2014, page 14, para 1.38.

16 Ofgem, OFT, CMA (2014), State of the Market Assessment, 27 March 2014, page 13, para 1.35.

Featured News

EU Conducts First-Ever Raids on a Company Under Foreign Subsidies Regulation

Apr 23, 2024 by

CPI

FTC Moves to Ban Non-Compete Agreements, Aiming to Boost Labor Mobility

Apr 23, 2024 by

CPI

Federal Judge Nods at $418M Deal in Real Estate Antitrust Suit

Apr 23, 2024 by

CPI

Mexican Watchdog Probes Amazon and Mercado Libre Over Loyalty Bundles

Apr 23, 2024 by

CPI

Competition Commission of India to Probe AI Landscape for Competition

Apr 23, 2024 by

CPI

Antitrust Mix by CPI

Antitrust Chronicle® – Economics of Criminal Antitrust

Apr 19, 2024 by

CPI

Navigating Economic Expert Work in Criminal Antitrust Litigation

Apr 19, 2024 by

CPI

The Increased Importance of Economics in Cartel Cases

Apr 19, 2024 by

CPI

A Law and Economics Analysis of the Antitrust Treatment of Physician Collective Price Agreements

Apr 19, 2024 by

CPI

Information Exchange In Criminal Antitrust Cases: How Economic Testimony Can Tip The Scales

Apr 19, 2024 by

CPI