Vertical Mergers and Input Foreclosure When Rivals Can Substitute Inputs: Safe Harbor for Low Share of Input Sales to Rivals?

By Serge Moresi & Marius Schwartz*

A vertical merger between a firm and an input supplier to that firm can generate efficiencies by eliminating double marginalization or alleviating other contracting inefficiencies. However, when the supplier also sells to that firm’s rivals, a key antitrust concern is input foreclosure: the merged firm might raise its input prices to downstream rivals, or otherwise degrade their access to the input, so as to raise rivals’ costs and increase its own profit from output sales. In some such cases, consumers in the downstream market also may be harmed. Concerns with input foreclosure featured prominently in high-profile vertical mergers such as Comcast/NBCU (2011) and AT&T/Time Warner (2018), where opponents alleged that the merged firm would use its video programming assets to disadvantage rival video distributors.1 Ongoing concerns with foreclosure are also manifest in the Vertical Merger Guidelines issued on June 30, 2020 by the U.S. Department of Justice and Federal Trade Commission (hereafter, “VMG”).2

The U.S. antitrust agencies assess the risk of foreclosure by considering whether the merged firm has both the ability to impede rivals significantly and the incentive to do so (VMG, pp. 4-5). In searching for observable metrics to guide this assessment, a plausible intuition is that foreclosure risk is low when the input supplied by the merged firm can be substituted (imperfectly) with other inputs supplied by upstream rivals and constitutes a small share of total inputs purchased by downstream firms pre-merger. One might then expect the merged firm to have only weak ability to impede downstream rivals.

The weak-ability point is not always correct. (a) An input may comprise a low share of a downstream firm’s input costs — even if the input is supplied by a monopolist — because of the firm’s ability to reduce the input quantity if its price rises by substituting to other inputs; yet (b) by raising the input price sufficiently, the input supplier still can have the ability to increase the firm’s marginal cost substantially, decimating its competitive position. Properties (a) and (b) can coexist whether an input is “essential” as in our example below or non-essential (i.e., production is possible even with zero quantity of that input) as in an extension of our analysis elsewhere.3

Moreover, and importantly, a low share of input costs magnifies the foreclosure incentive. A low such share implies that the vertically merged firm has a low share of input sales to downstream rivals and, hence, cannot extract much revenue from input sales to them. It then has relatively little to lose by foreclosing their access to its input, partially or completely, in order to raise their costs and gain profit from selling its own output. Thus, it is a priori ambiguous whether a low share of input sales to rivals should weaken or strengthen concerns with input foreclosure.4

In this note, we present an analytic example where foreclosure occurs post-merger only if the merged firm’s share of input sales to downstream firms is low rather than high.5 When the share is very high, the merged firm lowers the input price charged to the downstream rival and therefore there is no foreclosure.6 For intermediate values of the share of input sales, the merged firm raises the input price, leading to partial foreclosure. For very low shares, the merger results in complete foreclosure. In a subset of the foreclosure cases, consumers are harmed and in a smaller subset, total welfare — consumer welfare plus industry profits — also declines. By contrast, for intermediate or high shares of input sales, the merger increases total welfare and consumer welfare: the beneficial effect of eliminating double marginalization (“EDM”) outweighs the harmful effect from raising rivals’ cost (“RRC”) where present (as noted, for high shares, the input price falls post-merger instead of rising).7 In the example, therefore, a safe harbor for mergers where the upstream merging firm’s share of input sales is sufficiently low would work in the wrong direction. Foreclosure concerns are strongest when this share is low.

We do not wish to overstate the generality of this finding. While our example is not rigged — it uses standard modeling assumptions from the economics literature on industrial organization and antitrust — different assumptions about the downstream production technology might reverse our finding. Nevertheless, the force we identify is intuitive: a low share of input sales to a downstream rival reduces the merged firm’s loss from restricting input sales to that rival, thereby increasing the incentive to foreclose. Thus, our analysis suggests the need for caution in using a low share of input sales as a safe harbor in all circumstances.

Analytical Framework

Consider two downstream firms, D1 and D2, that produce and sell differentiated substitute products to consumers, at prices and , respectively. For simplicity, we assume that D1 and D2 are symmetric firms, that is, they face symmetric demand functions8 and use the same production technology. Production requires two inputs, X and Z. Input X is supplied to D1 and D2 by an upstream monopolist, firm U, at prices W1 and W2, respectively.9 Input Z is supplied by a fringe of competitive firms at a constant price of 1.10

We assume a Cobb-Douglas production function with a share parameter denoted by .11 When , each firm uses only input X; whereas for , each firm uses only input Z. In both of these polar cases, substitution between the inputs is not possible, and the production technology boils down to the familiar case of fixed proportions, where one unit of output always requires one unit of the relevant input. By contrast, for between 0 and 1, imperfect substitution is possible between the two inputs in response to changes in their relative price. For the Cobb-Douglas production function, the parameter equals the share of input X in a firm’s total cost of the two inputs. That is, given any price set by firm U for its input X, the input quantities chosen by a downstream firm to minimize its cost of producing a given output level will yield U a share of that firm’s total expenditure on the two inputs. Since D1 and D2 use the same production function, the parameter also equals the monopolist’s (revenue) share of input sales to the two downstream firms.

Pre-merger, U sets input prices and to D1 and D2, respectively.12 Given these input prices and the implied marginal costs, D1 and D2 compete downstream by setting output prices ( and , respectively) to consumers, with each firm choosing its price to maximize its own profit.13 These prices determine the downstream outputs and ultimately also input quantities.

Next, consider a merger between the input monopolist, U, and a downstream firm, say D1, to form a vertically merged firm U/D1. The merged firm now sets only the input price to D2, as the input price to D1 no longer plays a role (it is a purely internal transfer).14 Then, D1 and D2 set downstream prices as before, but D1 now sets to maximize the integrated profit of U/D1, from its own downstream sales and from input sales to D2. (As before, D2 sets to maximize its own profit.) The input price charged to the downstream rival (D2) is chosen at the outset to maximize the integrated profit of U/D1, anticipating how affects downstream prices and hence output sales by D1 and input sales to D2.

Our analysis focuses on how the parameter , that is, U’s share of input sales, influences the effects of the merger of U and D1on relevant variables: the rival’s input price and its downstream output ; consumer welfare CW; and total welfare TW (consumer welfare plus industry profits). For all values of , the merger increases the joint profit of the merging firms (compared to the sum of their individual profits pre-merger) and decreases the profit of D2, the input-customer-cum-downstream-rival.

Results

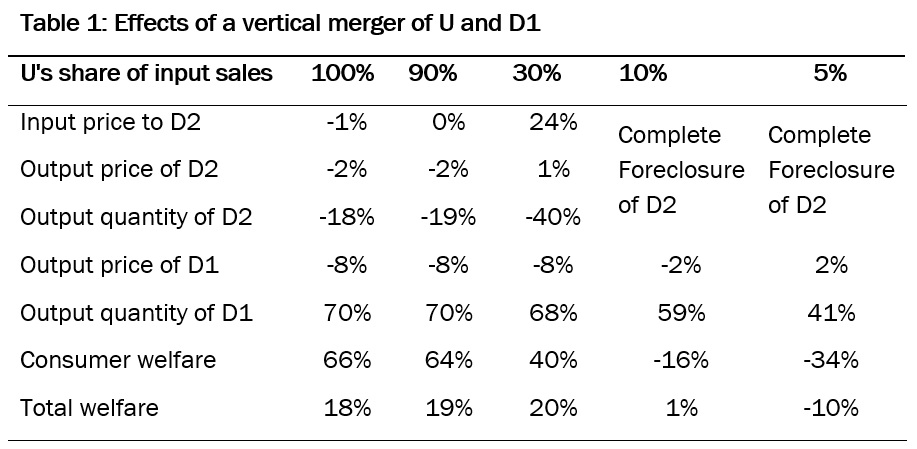

Table 1 shows the results for the case where the downstream firms, D1 and D2, face symmetric linear demand for their differentiated products and where the diversion ratio between the two products is equal to 50 percent.

As shown in the first column of Table 1, when U’s share of input sales is 100 percent (that is, U is an unconstrained input monopolist that faces no competition from other suppliers), the merger of U and D1 is procompetitive. There is no foreclosure since the input price charged to D2 falls, albeit only by 1 percent. The prices paid by consumers fall by 2 percent and 8 percent for D2’s product and D1’s product, respectively. The price reduction is larger for D1’s product than for D2’s product because the merger’s elimination of double marginalization (EDM) corresponds is tantamount to a larger cost reduction for D1 than the input price reduction to D2. As a result, D1’s output increases by 70 percent while D2’s output falls by 18 percent. Consumer welfare and total welfare increase by 66 and 18 percent, respectively.15

By contrast, the last column of the table shows that merger is anticompetitive when U’s share of input sales is 5 percent. The merged firm completely forecloses D2.16 Consumers no longer can purchase D2’s product and the price of D1’s product rises by 2 percent. D1’s output increases by 41 percent but D2’s output decreases by 100 percent since D2 is completely foreclosed. As a result, consumer welfare and total welfare decrease by 34 and 10 percent, respectively.

The other columns of Table 1 show the merger effects for intermediate values of U’s share of input sales. When the share is 90 percent, the merger leads to similar procompetitive effects as when the share is 100 percent, except that the merged firm keeps the input price charged to D2 at the same level as pre-merger (as opposed to reducing it). When U’s share of input sales is 30 percent, there is partial foreclosure since the merged firm raises the input price to D2, by 24 percent above the pre-merger level, yet the merger is beneficial for both consumer welfare and total welfare due to the EDM effect. Finally, when U’s share is 10 percent the merger leads to similar anticompetitive effects as when the share is 5 percent: the merged firm completely forecloses D2 and consumer welfare falls. Unlike the case with a 5 percent share, the price of D1’s product now falls and total welfare increases, although those effects are small.

To summarize, in our example the degree of foreclosure — represented by the percentage increase in the input price to the rival — is greater when the input supplied by the merged firm accounts for a smaller rather than larger share of the rival’s input costs. And with complete foreclosure, the merger reduces consumer welfare as well as total welfare. Our findings also illustrate, however, the familiar point that harm to competitors does not imply harm to consumers, since the rival’s profit declines in all cases whereas consumer welfare can increase substantially.

Stepping beyond our specific example, our analysis cautions against using a low share of input sales as a universal safe harbor for vertical mergers. While a low share may reduce the merged firm’s ability to foreclose, it also magnifies the foreclosure incentive because the merged firm cannot extract much revenue from input sales to rivals and, hence, its loss from foreclosing rivals is low.

Click here for a PDF version of the article

* Moresi: CRA International, Inc., Washington DC 2004 smoresi@crai.com. Schwartz: Department of Economics, Georgetown University, Washington DC 20057 mariusschwartz@mac.com. We thank Martino De Stefano, Michael Katz, John Rust, and Steve Salop for helpful discussions. Any errors are ours alone.

1 See, e.g. William P. Rogerson, A Vertical Merger in the Video Programming and Distribution Industry: The Case of Comcast-NBCU, in THE ANTITRUST REVOLUTION 534 (John Kwoka & Larry White eds., 6th Ed., 2014); the Memorandum Opinion of Judge Richard J. Leon in United States v. AT&T and Time Warner, June 12, 2018, at https://ecf.dcd.uscourts.gov/cgi-bin/show_public_doc?2017cv2511-146. See also the Memorandum Opinion of Judge Richard J. Leon in United States v. CVS and Aetna, September 4, 2019, at https://ecf.dcd.uscourts.gov/cgi-bin/show_public_doc?2018cv2340-135.

2 “A vertical merger may diminish competition by allowing the merged firm to profitably use its control of the related product to weaken or remove the competitive constraint from one or more of its actual or potential rivals in the relevant market. For example, a merger may increase the vertically integrated firm’s incentive or ability to raise its rivals’ costs by increasing the price or lowering the quality of the related product.” (VMG, p. 4) A related product is defined as “a product or service that is supplied or controlled by the merged firm and is positioned vertically or is complementary to the products and services in the relevant market. For example, a related product could be an input, a means of distribution, access to a set of customers, or a complement.” (VMG, p. 2, emphasis added.) These competitive concerns are elaborated in VMG, Section 4.a, titled Foreclosure and Raising Rivals’ Costs, pp. 4-10. Footnote 4 on p.4 notes that “For ease of exposition, the principal discussion is about input foreclosure.”

3 Serge Moresi & Marius Schwartz, Vertical Mergers with Input Substitution: Double Marginalization, Foreclosure and Welfare, in progress (available on request).

4 In “foreclosure” we include (i) complete foreclosure, where the merged firm stops supplying the input to a rival (which in our example drives the rival’s output to zero, though this property is not general), and (ii) partial foreclosure, where the merged firm raises the input price to a rival and the rival remains active but with reduced output. The VMG refer to (i) as “foreclosure” (refuse to supply to rivals) and to (ii) as “raising rivals’ costs.” See VMG, p. 4.

5 The example draws on Moresi & Schwartz (2020), supra note 3.

6 The output of the downstream rival still falls post-merger because, as a result of eliminating double marginalization, the merged firm is a more efficient competitor than the downstream merging firm was pre-merger. For the polar case where the merged firm’s share of input sales is 100 percent, see, e.g. Shihua Lu, Serge Moresi & Steven C. Salop, 2007, A Note on Vertical Mergers With an Upstream Monopolist: Foreclosure and Consumer Welfare Effects, mimeo, Charles River Associates, http://www.crai.com/sites/default/files/publications/Merging-with-an-upstream-monopolist.pdf. See also Appendix B in Steven C. Salop, Carl Shapiro, David Majerus, Serge Moresi & E. Jane Murdoch, 2003, News Corporation’s Partial Acquisition of DIRECTV: Economic Analysis of Vertical Foreclosure Claims, report submitted to the Federal Communications Commission on behalf of GM/Hughes and News Corporation, http://apps.fcc.gov/ecfs/document/view.action?id=6514283359.

7 Our results are derived by assessing the potential harm from (full or partial) foreclosure and the potential benefits from the elimination of double marginalization in a common equilibrium-analysis framework.

8 We assume linear demand. The demand for D1’s product is , and that for D2’s product is . The implied diversion ratio from one product to the other is 50 percent.

9 We assume upstream monopoly instead of imperfect competition in order to simplify the analysis.

10 Our framework is similar to Roman Inderst & Tommaso Valletti, Incentives for Input Foreclosure, 55 EUR. ECON. REV. 820 (2011). They assume a different production technology and focus on the relationship between pre-merger margins and incentives to engage in complete foreclosure post-merger.

11 Formally, , where is the quantity of output, and are the quantities of the two inputs, is a scale factor, and is the share parameter. We set so that the total cost function is given by , where marginal cost is . For a given value of , a firm’s marginal cost is higher when the monopoly input’s price is higher. For a given value of , an increase in the value of implies that a firm’s marginal cost decreases if and increases if , that is, an increase in the monopolist’s share of input sales leads to an increase in the marginal cost of a downstream firm if and only if the price of the monopoly input is higher than the price of the competitively supplied input. In our simulations we will set the monopolist’s marginal cost equal to 1, hence the monopoly input price will always exceed 1.

12 We assume linear prices, as in Examples 2, 3, and 6 in the VMG. For the polar case with , the merger effects with two-part tariffs for the input (rather than linear prices) are reported in Table 4 of the Online Appendix of Serge Moresi & Marius Schwartz, Strategic Incentives When Supplying to Rivals With an Application to Vertical Firm Structure, 51 INT’L J. INDUS. ORG. 137 (2017). The Online Appendix is also available as Appendix B at https://ssrn.com/abstract=2890503.

13 The resulting output prices form a standard Bertrand/Nash equilibrium. In particular, we assume that input prices are public information when downstream firms set output prices. For a framework where input prices are private information, see, e.g. the Online Appendix of Serge Moresi & Steven C. Salop, vGUPPI: Scoring Unilateral Pricing Incentives in Vertical Mergers, 79 ANTITRUST L. J. 185 (2013), http://www.americanbar.org/content/dam/aba/publishing/antitrust_law_journal/at_alj_moresi_salop.pdf.

14 D2’s marginal cost is equal to , and D1’s marginal cost is equal to 1 (D1 obtains input X at U’s marginal cost of 1 and purchases the competitive input also at this price). See supra note 11.

15 Similar procompetitive effects also occur when D1 and D2 face asymmetric linear demand functions that satisfy Slutsky symmetry. See Lu et al. (2007), supra note 6.

16 With a Cobb-Douglas technology, each input is essential. The merged firm thus completely forecloses D2 by refusing to deal with D2 or charging a prohibitively high input price to D2. Complete foreclosure can occur also when the input is non-essential. Moresi & Schwartz (2020), supra note 3.

Featured News

DOJ and FTC Introduce Website for Reporting Anti-Competitive Healthcare Practices

Apr 18, 2024 by

CPI

US Congress Advances Legislation to Compel TikTok Sale

Apr 18, 2024 by

CPI

UK Financial Sector Advocates Enhanced Regulatory Accountability

Apr 18, 2024 by

CPI

Google and All 50 States Defend $700 Million Consumer Settlement

Apr 18, 2024 by

CPI

Colorado Enacts First Law to Protect Consumer Brainwave Data

Apr 18, 2024 by

CPI

Antitrust Mix by CPI

Antitrust Chronicle® – Economics of Criminal Antitrust

Apr 19, 2024 by

CPI

Navigating Economic Expert Work in Criminal Antitrust Litigation

Apr 19, 2024 by

CPI

The Increased Importance of Economics in Cartel Cases

Apr 19, 2024 by

CPI

A Law and Economics Analysis of the Antitrust Treatment of Physician Collective Price Agreements

Apr 19, 2024 by

CPI

Information Exchange In Criminal Antitrust Cases: How Economic Testimony Can Tip The Scales

Apr 19, 2024 by

CPI